Golar LNG: Changing Business Model Creates Opportunity For Investors (NASDAQ:GLNG)

alvarez/E+ via Getty Images

On Wednesday, April 6, 2022, liquefied natural gas transportation firm Golar LNG Limited (NASDAQ:GLNG) announced that it was selling about a third of its stake in New Fortress Energy (NFE). Golar LNG intends to use the proceeds to fund the development of floating liquefied natural gas platforms. This is not exactly surprising as I have discussed in various previous articles (such as this one) how profitable this division could ultimately prove to be for the company.

Admittedly, the coronavirus pandemic set it back somewhat as a result of the legal fight with BP p.l.c. (BP) but everything appears to be back on track now. Admittedly, the current energy crisis in Europe may do wonders for its attractiveness. This decision to raise capital to fund the development of its floating platform business could ultimately prove to be a very powerful growth engine for Golar LNG over the next several years.

About The Deal

As stated in the introduction, Golar LNG stated that it sold about a third of the 18.6 million shares of New Fortress Energy that it has owned for about a year. Admittedly, Golar LNG did not state when it sold these shares. This is certainly not atypical, as companies do not usually announce large trades like this right away. Rather, they usually conduct the sale gradually over a period of time and then announce it after the fact in order to avoid affecting the market price too much.

Golar LNG first acquired these units back in April 2021, when it sold its Hygo Energy joint-venture to New Fortress Energy (NFE) in exchange for $580 million and 31,372,549 shares of New Fortress Energy common stock. As Golar LNG owned half of Hygo Energy, it received half of the proceeds. The company also sold its entire stake in Golar LNG Partners in a related transaction.

This had the very positive effect of streamlining the company and giving it a nice infusion of cash, which Golar LNG desperately needed around that time. Admittedly, the company’s stake in Hygo Energy never made a great deal of sense, as that business was primarily a power generation and utility firm, which is vastly different from the rest of Golar LNG’s business. As a result of this transaction, Golar LNG is primarily focused on the operation of tankers and other floating offshore liquefied natural gas platforms, which is the company’s core competency.

About The Floating LNG Plant Business And Growth

As stated in the introduction, Golar LNG expects this transaction to net it about $250 million in cash that it can use to further the construction of floating liquefaction plants. This is a business unit that has been proving to be a remarkably successful one for the company so far. It is also poised to be a major growth engine for the company. We can see this quite clearly by looking at the business unit’s recent results.

Golar LNG currently only has a single operating floating liquefaction plant, the FLNG Hilli. This vessel alone generated revenue of $56.406 million in the fourth quarter of 2021. This is, interestingly, more than the $52.440 million that was generated by all of the ships in the company’s transportation fleet. This is not exactly unusual, as I have pointed out in various past articles on Golar LNG how this vessel alone is quite often very comparable to the rest of the company’s fleet combined.

The FLNG Hilli also tends to enjoy much more stable financial performance than the remainder of the company’s fleet. This is largely a virtue of its very long-term multi-year contract. This contract guarantees that the plant will receive a certain baseline level of revenue regardless of energy prices or macroeconomic conditions. We can actually see this by looking at the revenues generated by the unit in the fourth quarter of 2020 and comparing them to 2021.

|

Q4 2021 |

Q3 2021 |

Q4 2020 |

|

|

FLNG Revenue |

$56,406 |

$54,480 |

$62,489 |

(all figures in thousands of U.S. dollars)

This is certainly much more attractive to long-term investors than the rest of the fleet. The liquefied natural gas carriers tend to have much shorter contracts that may only be for a single voyage. This makes them much more vulnerable to changes in the macroeconomic environment.

We saw this in 2020. As industry followers likely know, the liquefied natural gas market collapsed in 2020 along with energy prices (although government restrictions on transportation played a role in this too). Golar LNG saw this in the fact that the company’s time-charter equivalent (a shipping industry performance measure meant to compare the fleet’s revenue performance despite differences in contract type and length) was 17% higher in the fourth quarter of 2021 than in the prior-year quarter. This is the reason why the shipping fleet’s adjusted EBITDA increased by $10.388 million over the period.

In addition, the liquefied natural gas market is seasonal by its very nature. This is mostly because natural gas is primarily used as a heating fuel, so it sees its biggest demand during the winter months. Thus, the fourth quarter is typically the strongest, as importers work to build their stockpiles of natural gas in preparation for the heaviest usage months; imports are typically weaker during other seasons. This only adds to the volatility that natural gas shipping companies see in their earnings.

This earnings variability has long been something that many have been concerned about with regard to the company, particularly when we see periods of steep weakness in the industry. So, the stability of revenues from the floating liquefaction business is something that will likely bring some comfort.

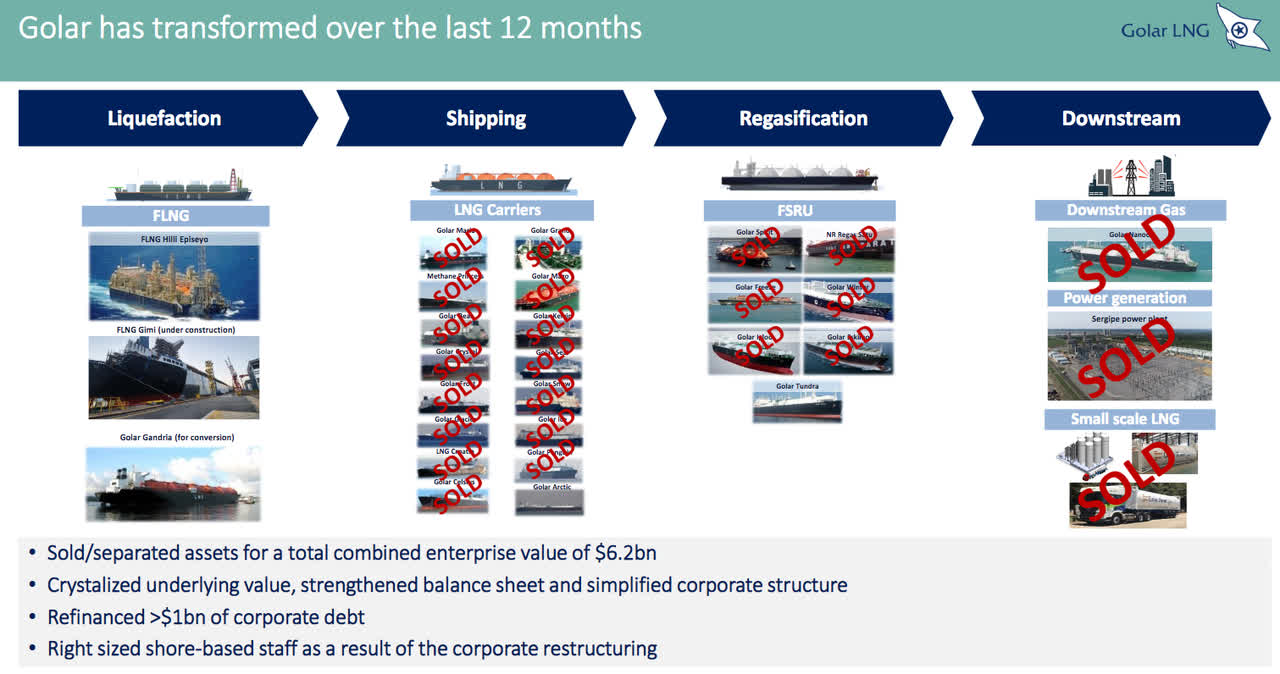

With that said, Golar LNG appears to be transitioning out of the traditional shipping industry, at least partially. On April 6, 2022, an entity called CoolCo completed the acquisition of eight liquefied natural gas carriers from Golar LNG. This leaves Golar LNG with only the Golar Arctic as its final remaining tanker.

Golar LNG Investor Presentation

Golar LNG is thus focusing its efforts on its floating liquefaction plants, which will likely make the company’s revenues far more stable than they were prior to the coronavirus crisis. However, Golar LNG does still own 31.2% of CoolCo so it does still have significant exposure to the shipping market. It is still worth keeping in mind, though, that the sale of these ships did help shore up Golar’s balance sheet and reduced its overall exposure to the vagaries of the shipping market.

We can also see that the company is going to be expanding its fleet of floating liquefaction plants in the near future. The first of these is the Golar Gimi, which is currently scheduled to begin operation in 2023. This vessel has already received a twenty-year contract from BP, which is quite nice to see. The reason for this is that it effectively ensures that the vessel will begin generating revenue as soon as it is operational.

Thus, Golar LNG is not spending a great deal of money to construct a facility that nobody wants to use. The fact that Golar LNG has a contract in place also allows it to have a reasonably certain idea of how profitable the FLNG Gimi will be. Golar LNG has stated that the earnings from the FLNG Hilli and FLNG Gimi together could result in a quadrupling of the earnings currently generated by this segment of the fleet by 2026. When we consider that the business unit already generates more than half of the company’s earnings, we can clearly see the growth potential here. It is uncertain whether or not the market is actually recognizing this. As we will see shortly, there is reason to believe that it is not.

Another thing that we can see above is that Golar LNG has listed a third floating liquefaction plant above, the FLNG Golar Gandria. This vessel has not yet begun construction, however. In fact, Golar LNG has not yet received a contract for it, so it does not make any sense for it to begin construction until it knows for sure that it will be able to contract out the facility and thus make money on it. It is reasonable to assume that it might be able to get one though, particularly considering the desperation that Europe is currently displaying for liquefied natural gas. If Golar LNG does ultimately manage to secure a contract for this third floating liquefaction plant, it is quite easy to see how this could result in a phenomenal growth opportunity for Golar LNG.

Fundamentals Of Liquefied Natural Gas

Golar LNG’s ability to secure a new contract for the FLNG Hilli once the current one expires in 2026 ultimately depends on the global demand for liquefied natural gas. The same could be said for the company’s ability to obtain a contract for the FLNG Golar Gandria.

Fortunately, the fundamentals are quite positive, and they may have even become more positive due to the tensions between Russia and the European Union. For those that are unaware, the European Union imports an enormous amount of natural gas from Russia due to the fact that the continent consumes a large and growing amount of the compound but its own resources are lacking. In fact, the continent would need to import 115 million tons of liquefied natural gas annually in addition to what it already imports just to replace the gas that it imports from Russia. When we consider that the current global production of the compound is only about 400 tons, we can see the potential for market growth here, if Europe tries to get away from its dependence on Russia.

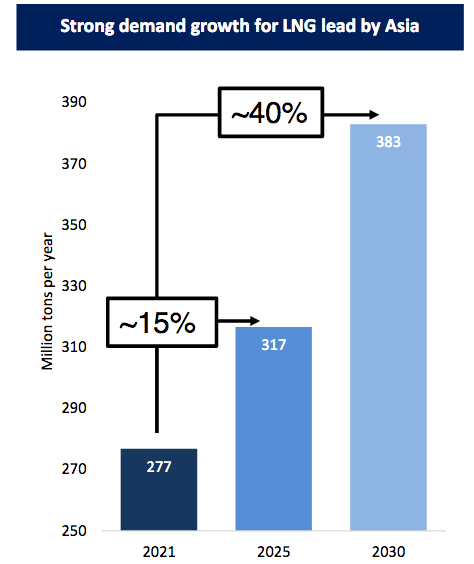

Currently, though, Asia is expected to drive growth in the liquefied natural gas market. Indeed, the continent is expected to increase its demand by 40% between now and 2030.

GLNG Investor Presentation

This growing demand for the substance is being driven by international concerns about climate change. This has prompted the governments of many nations to take a variety of actions that are meant to reduce the carbon emissions of their respective nations.

One of the easiest ways to do that is by switching from coal to natural gas for many tasks. This is because natural gas burns much cleaner than coal for most tasks and is reliable enough to support a modern electric grid, unlike renewables. As natural gas is, as the name implies, a gas, it requires the use of specialized facilities to convert it into a liquid for transportation across bodies of water. This is exactly what is done at the floating liquefaction plants that Golar LNG operates. Thus, the growing demand for natural gas from both Asia and Europe should result in the growing demand for the company’s plants and thus make it easier to obtain contracts.

Valuation And Stock Price

Over the past year, Golar LNG has seen tremendous share price appreciation, with the company’s stock climbing a remarkable 129.34%.

Seeking Alpha

We do note, though, that much of the gain was since the start of the year, so it is certainly possible that this is due to the market seeing that the liquefied natural gas shipping market is improving. It is also possible that investors are much more optimistic about the company’s future than analysts.

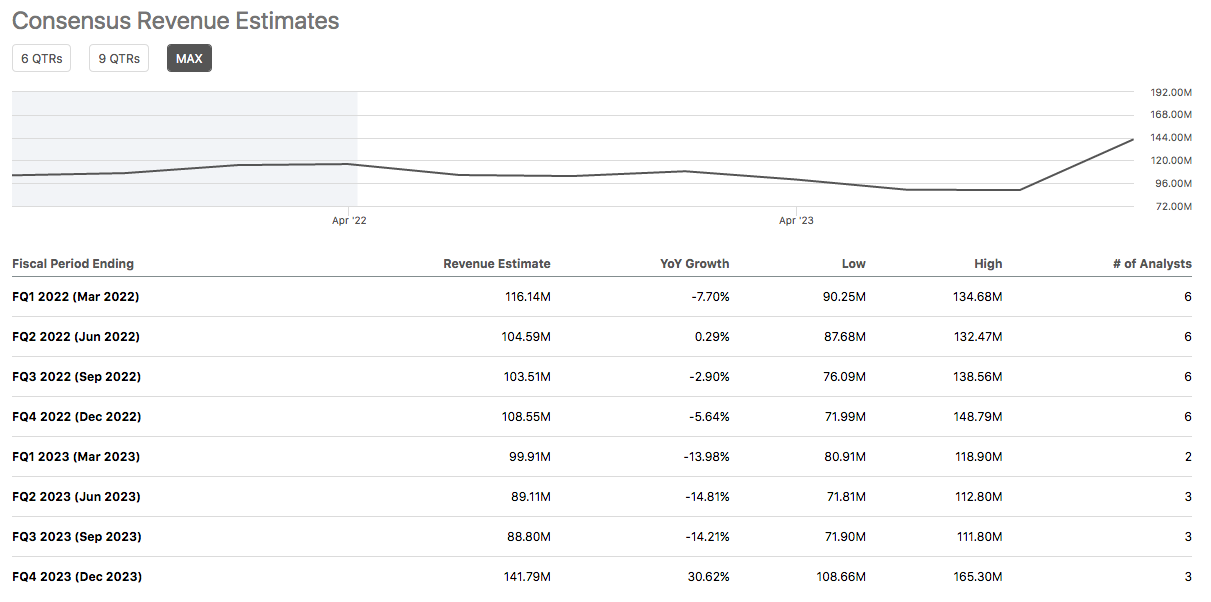

Golar LNG trades at a forward price-to-earnings ratio of 28.75 as of the time of writing. However, this forward price-to-earnings ratio is based on the current expectations of analysts, which appear to be too low. Indeed, analysts currently expect that Golar LNG’s earnings will decline in almost every quarter between now and the end of 2023 on a year-over-year basis.

Seeking Alpha

The only quarter in which significant earnings growth is foreseen is the fourth quarter of 2023. The FLNG Gimi is expected to be the most significant driver of growth during 2023 as we have already discussed. It is admittedly uncertain when this unit will begin operation, though, as management has only stated that it will start operation “during the second half of 2023.” Thus, it is possible that the unit will actually start operation earlier than the fourth quarter as analysts expect. If that is the case, then the stock would actually be cheaper than the current quoted figure of 28.75.

With that said, though, the true story here is over the 2024 to 2026 period, as that will be the time in which both floating liquefaction plants are active. As already mentioned, the earnings produced by the company’s floating liquefaction plant unit could nearly quadruple. Thus, we could very easily see the company’s overall earnings triple or more over the coming four-year period. At less than 30 times 2023 earnings, this company looks reasonably cheap.

Conclusion

In conclusion, Golar LNG may currently be offering much more than the market gives it credit for. In particular, we are looking at a company that has been making great strides at changing its business model, potentially tripling or quadrupling its earnings over the next four to five years. As the stock is currently trading for less than thirty times next year’s earnings, despite its already strong gains, there could be a very real possibility of getting into an incredible opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.